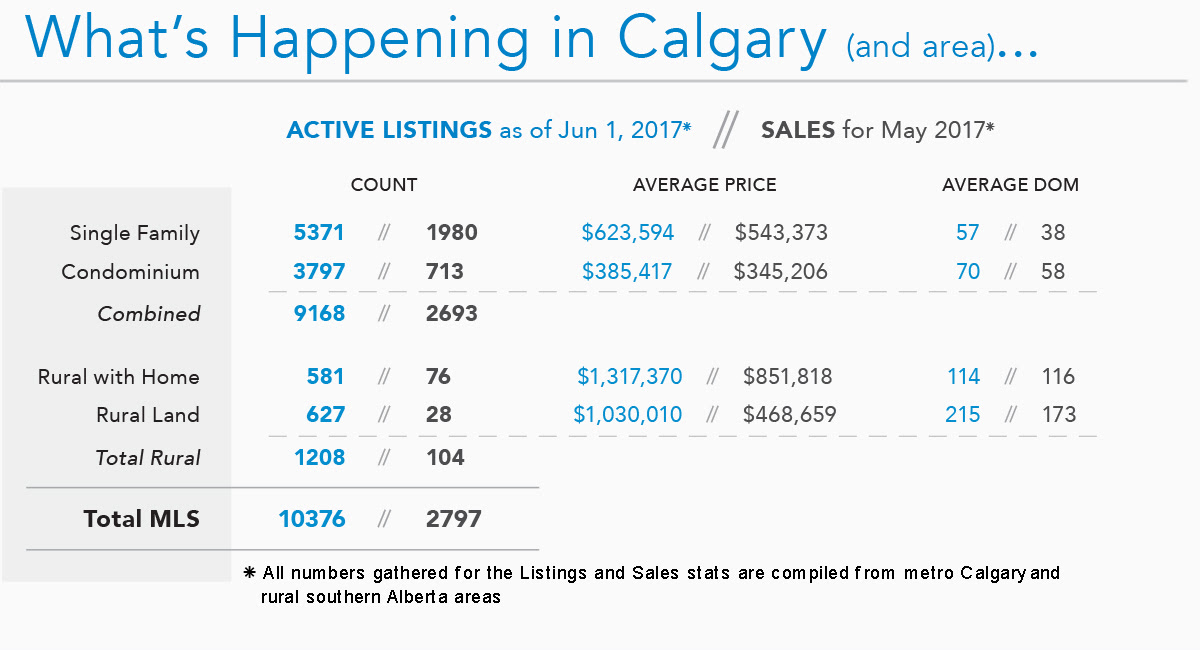

Because a Great Experience Begins with a Great Agent

Deprecated: Creation of dynamic property TotalCMS\Component\Blog::$root_offset is deprecated in /home/jbosti5/public_html/kerrybostick.com/rw_common/plugins/stacks/total-cms/TotalCMS/Component/Component.php on line 76

Five Considerations for Purchasing a Condo When purchasing a condo, there are many things to consider to ensure better re-sale conditions down the road.

1 Purchase the largest unit that you are able to afford. Two bedroom condos are much more desirable and are easier to re sell than one bedroom suites and studios.

2 You will pay extra for a unit with a view, but so will the next person who buys. Having a view is a great differentiating point in condos.

3 Avoid units that are beside or across from an elevator, that overlook garbage areas or the coming and goings of heavy vehicle traffic, or are positioned over the garage entrance. You want to avoid bad sights and loud noises.

4 Make sure you get a parking space. Even if you don’t drive, you can rent it out. Having a storage locker is also highly encouraged since there is rarely enough storage space in a condo unit.

5 Ensure the aroma and maintenance of the common areas, such as the lobby, hallways and stairwells are pleasant and clean.

How Do Home Equity Loans in Canada and Lines of Credit Compare? A home equity loan [HEL] and a home equity line of credit [HELOC] allow you to borrow money against your home as collateral. These loans can be taken out to meet expenses such as home repairs and renovations, financing a new property or funding your child’s college education. It is a good idea to understand how these two loans work if you are looking to use the equity in your home. Whether you go for a HELOC or home equity loan Canada or anywhere in the United States, you should know the basics, advantages and disadvantages of these loans.

HOW THEY WORK: Both HEL and HELOC are secured loans where you pledge your property to the bank or lender. In case you fail to repay the loan, the bank/lender can lay claim on your property.

In a HEL, banks offer a large amount of money (close to 80% of the value of your property) in one shot as they are secured loans. A home equity loan is typically offered at a low rate of interest, making it reasonably affordable.

On the other hand, a home equity line of credit is a revolving credit line secured against your home as collateral. A maximum amount, based on your home’s built-up equity, is made available by the lender. You can draw from this credit line whenever you need cash.

REPAYMENT: A HELOC has a term ranging from 5–25 years and the amount that the borrower withdraws can be repaid by the end of that term, either in part or at one shot. Interest is charged only on the amount that is used by the borrower and not the whole amount available in the account.

Contact CIR REALTY Now For A Free Market Evaluation. Our goal is to meet all of your real estate needs. We look forward to hearing from you. We are happy to answer ANY questions you may have. [email protected] | 403-837-5377